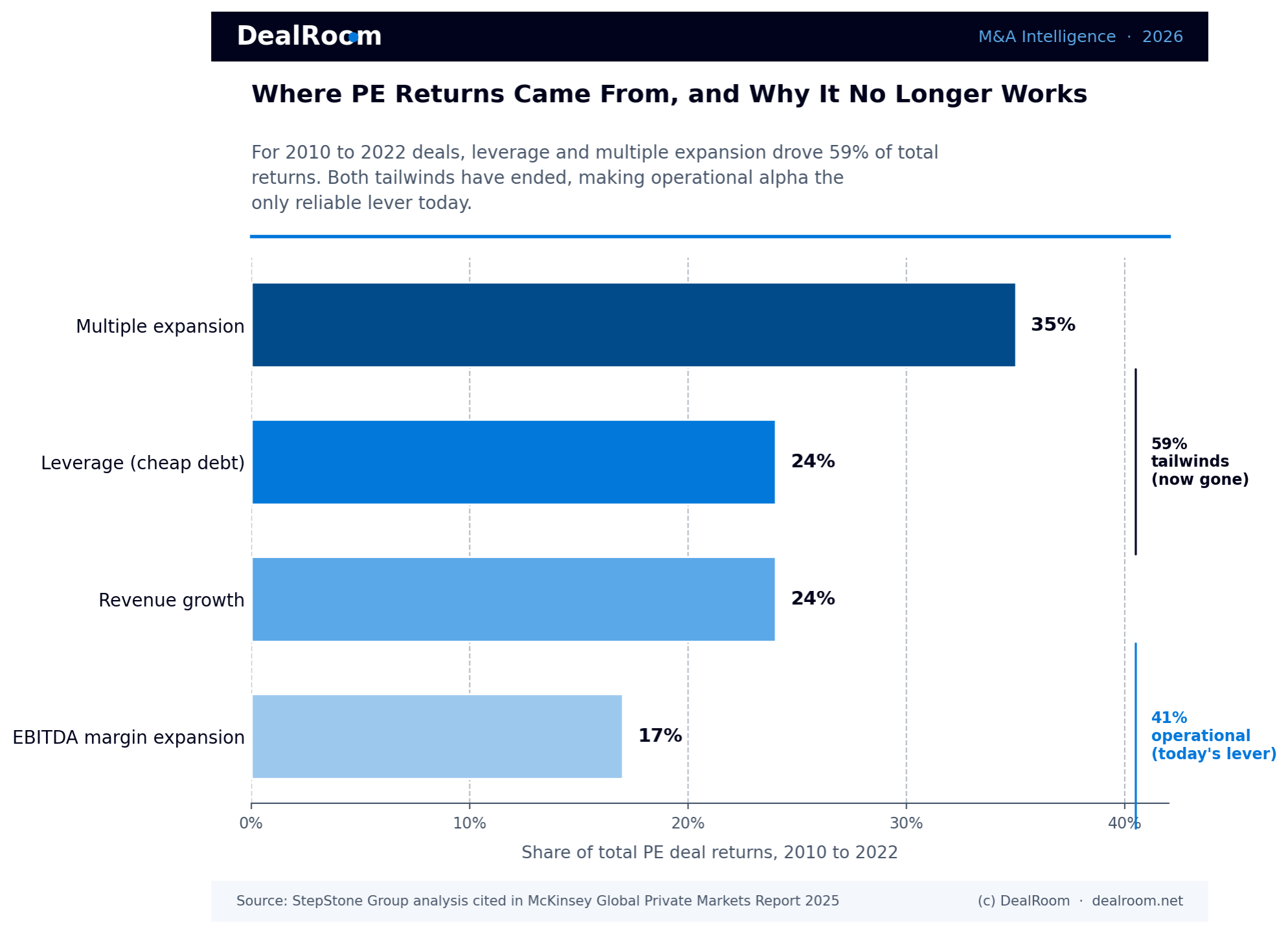

The median private equity hold period reached nearly 6 years in 2025, the longest in 25 years of tracking, according to Private Equity Info, while Bain's 2026 Global Private Equity Report concludes that PE firms now need roughly 12% annual EBITDA growth (vs the historical 5%) to deliver the benchmark 2.5x return over five years. The cheap-leverage and multiple-expansion tailwinds that produced 59% of PE returns from 2010 to 2022 (StepStone analysis cited in McKinsey 2025) are gone. Today, value creation has to come from operational alpha, and the table and chart below show exactly which levers move the needle.

DealRoom

35 Largest M&A Deals · 2026

Filter, sort, and explore.

Search Sector Decade Outcome

Key Definitions

Value creation

The process of growing a portfolio company's value during the PE hold period through operational, financial, and strategic improvements.

Operational alpha

The excess return generated from improving how a business runs, separate from financial engineering or market timing.

Multiple expansion

Selling a company at a higher EBITDA multiple than the purchase multiple. Often the largest single contributor to PE returns.

MOIC

Multiple on Invested Capital. Total cash returned to investors divided by capital deployed. A 3x MOIC means $3 returned for every $1 invested.

Private equity is in a new era of value creation. More than 28,000 companies sit in PE portfolios globally as of mid-2025, with a record share held longer than four years (Bain Global PE Report 2026). The tailwinds that contributed to easy profits have passed, which is why private equity firms must now create value through the business itself.

It is time for a new PE investment strategy. Managing the capital structure and planning for exit still factor into value creation for private equity, but given today's environment of lengthy holding periods, high purchase multiples, and rising performance pressures, they are not enough on their own. Sustainable, lasting operational enhancements are now crucial. Financial engineering can no longer account for most of the value created. Instead, private equity firms must focus on creating better businesses.

I’ve worked in M&A advisory for over a decade and have seen this shift firsthand. Through 400+ conversations with the PE operators, corp dev leaders, and integration specialists who've actually run these deals, the message is clear: If firms think they can win by being better financiers (capital structure, leverage, etc. ), they are mistaken. The era of strong leverage tailwinds and easy multiple expansion is over. The remaining path to create value is through actually making a business substantively more valuable while you own it. And most PE firms still don’t know what that means on an execution level.

What is Private Equity Value Creation?

Private equity firms buy companies with one goal in mind: selling them later for a profit. There are three sources of value creation that allow them to achieve this: operational improvements, financial engineering, and management during their holding period. That period of ownership is usually between three and seven years, though 2025 data shows median holds have lengthened to roughly 6 years (S&P Global). During that time frame, firms need to determine a robust set of initiatives to drive profitable top-line growth and deliver on execution. Execution is less about strategy and more about disciplined implementation.

Today's reality is that the old playbook is broken. Bain calls today's environment '12 is the new 5'. PE firms now need approximately 12% annual EBITDA growth (vs the historical 5%) to deliver the benchmark 2.5x return over five years (Bain Global Private Equity Report 2026). Previous vintages were able to rely more on financial leverage and market timing as value creation mechanisms. Both are still significant, but they don't operate independently.

Today's PE firms are far more focused on what's being called 'operational alpha' or the disciplined execution of initiatives to improve EBITDA through smarter processes, pricing, and execution. Whether you are on the buy-side, preparing to sell your business, or operating within a portfolio company, understanding these value creation levers and common points of execution failure can create a stark difference between the value you expect and the value you realize.

Core Principles of Private Equity Value Creation

Private equity firms have three primary drivers of returns for their portfolio companies: strategic, operational, and financial. Operational improvements lay the groundwork for sustainable growth and are executed by the management team. Financial engineering creates value through capital structuring and leverage. Strategic initiatives, including buy-and-build, reposition the business to command a higher exit multiple.

How Private Equity Creates Value

Private equity firms pull on multiple levers of value creation at once.

- Financial engineering involves capital structuring and using leverage to increase potential returns.

- Multiple arbitrage entails acquiring a company at one multiple and exiting at a higher multiple, typically due to market timing or changing the business focus of the company.

- Revenue growth can be achieved by entering new markets or developing new products. It can also be achieved by making acquisitions. In 2025, add-on acquisitions accounted for 73% of all PE buyout transactions and 75.9% in Q2 alone, the buy-and-build strategy now dominates the market (PitchBook / Cherry Bekaert 2025 PE Mid-Year Report).

- Cost optimization is the process of decreasing expenses without hurting the company's competitive advantage.

- Margin expansion can come from both pricing strategy and operational improvements.

Examples of value drivers include EBITDA improvements through revenue and cost synergies, valuation expansion through better positioning, debt reduction by paying down debt with cashflow, and strategic repositioning of the business tactic.

Top private equity firms depend less on external factors and more on repeatable processes. Many firms use data to make decisions and track success by objective measurements.

Role of Management Teams in Value Creation

Management is everything when it comes to value creation. Management teams are evaluated by private equity firms in their due diligence process and replaced if they lack the ability to execute. A good management team has deep industry expertise and operational expertise. They understand how to navigate change. Great teams can execute on strategy and produce tangible results.

Management teams often hire seasoned executives to fill gaps in sales, operations, or technology functions. Private equity firms and management must be aligned on the vision, milestones, and incentives. Management teams are typically granted equity to align their interests with those of the private equity investors. Reporting requirements and board seats help ensure everyone is on the same page.

Importance of Operational Efficiency

Operational efficiency drives sustainable value creation through reducing waste, improving productivity, and optimizing the use of resources. If you can deliver your product or service faster and cheaper than your competitors, you win the race.

Operational improvements can be made through manufacturing operations, supply chain, and service delivery. Investments in technology can help automate tedious tasks and provide better information for decision making. Tighter working capital management improves your cash position by smarter management of inventory, accounts receivable, and accounts payable.

Operational efficiency has a direct positive impact on EBITDA and cash flow. Unlike other discretionary expenses, these benefits are enduring because they strengthen the core of your business. Once you've streamlined operations so they can grow without incurring proportional costs, you've created your growth engine.

What is Operational Alpha?

Operational alpha is the excess return a private equity firm generates from improving how a portfolio company actually runs, separate from any financial engineering or market timing. The term originated in asset management in the early 2010s and has since migrated to private equity, where it now describes the disciplined execution of initiatives to grow EBITDA through smarter processes, sharper pricing, faster integration, and better data infrastructure.

In practice, generating operational alpha means embedding operating partners alongside management, instrumenting every part of the business with real-time KPIs, and treating each investment thesis as a falsifiable hypothesis to be tested in the first 100 days. Top-quartile PE firms now build dedicated portfolio operations teams (Apollo's APPS, KKR Capstone, Bain Capital's Portfolio Group) whose entire job is to manufacture operational alpha across the fund.

Why it matters now: with multiple expansion no longer a reliable tailwind, operational alpha is increasingly the only repeatable lever a fund can pull on. Bain's 2026 Global Private Equity Report concludes that today's deals require roughly 12% annual EBITDA growth to deliver historical return benchmarks, almost double the 5% that worked in the prior cycle.

What is a Value Creation Plan?

A value creation plan (VCP) is the playbook a private equity firm builds during diligence to lay out exactly how a portfolio company will grow its EBITDA and exit at a higher multiple than the entry price. Unlike a strategic plan, a VCP is operational, quantified, and time-bound. Every initiative has an owner, a measurable target, a budget, and a deadline tied to the hold period.

A complete VCP typically includes:

- Investment thesis: the one or two beliefs that justify the deal

- Value creation levers: the 4 to 7 specific initiatives that will drive EBITDA growth

- Owners: a single accountable person per initiative, ideally inside the management team

- KPIs and milestones: leading and lagging indicators with quarterly targets

- Budget: capital and operating expense allocations to fund each initiative

- Risks and dependencies: what could derail each lever and the mitigation plan

- Baseline metrics: agreed during diligence so progress can be measured against day one

- Exit path: which type of buyer the company is being prepared for and what they will value

The best VCPs are built collaboratively with management during the diligence period and then revisited at every quarterly board meeting. Top-quartile funds typically run 12 to 18 active VCP initiatives across a typical hold, with disciplined sunset and pivot decisions when a lever isn't working.

Key Value Creation Strategies and Levers

The four value drivers used by private equity firms to create equity value are operations, financial optimization, strategic growth, business continuity planning, and aligning management incentives. The implementation of each lever affects performance and valuation positively.

Operational Improvements and Process Optimization

Operational improvement may be your fastest route to sustainable value creation. There are almost always opportunities to improve operations where inefficiencies across business processes, the supply chain, and production are destroying margins. Process optimization includes cutting expenses while maintaining quality. Opportunities can include centralizing purchasing, automating business processes, and eliminating duplicate systems.

Operational improvements typically drive 50 to 250 basis points of EBITDA margin expansion in the first 24 months of a hold, with top-quartile funds delivering 300+ bps. There will typically be a mix of quick wins and longer-term value creation opportunities. Quick wins can include cost savings from renegotiating contracts with vendors, trimming excess locations, or halting budget drain from low ROI initiatives. Longer-term value can come from implementing lean manufacturing processes, streamlining your organization's culture, or modernizing your technology stack to make better data-driven decisions.

Revenue improvements can be realized through operational improvements as well. Better demand forecasting can lift revenue 2 to 4% in the first 12 months and frees inventory capital simultaneously (McKinsey Operations Practice). More efficient inventory management can free 5 to 20% of working capital. Quality control reduces write-offs.

Financial Engineering and Capital Structure

Financial engineering is all about restructuring your company's balance sheet to increase returns and lower your cost of capital. Adjusting the debt-to-equity mix, refinancing debt, and raising capital when market conditions are favorable are all aspects of financial engineering.

Decisions you make when you close your acquisition help determine your financial strategy. Selecting the right mix of senior debt, mezzanine, and equity can allow you to leverage your purchase while maintaining financial flexibility. Your capital structure should support your growth plans and not overload your company with risk.

There are many opportunities to create value through financial engineering as interest rates fluctuate and your company's credit rating improves. By refinancing to extend maturity profiles, reduce interest payments, and pay capital back to investors through dividends, you can increase your overall returns without impacting any operating metrics.

Strategic Growth and Buy-and-Build

In 2025, add-on acquisitions accounted for 73% of all PE buyout transactions, the highest share on record (Cherry Bekaert 2025 PE Report). Expansion doesn't always mean you're selling more widgets. Maybe you expand into new territories, add products, or go after market share. Opportunities may exist by finding new unserved or underserved customers.

Accelerate your growth with acquisitions. Faster than organic growth alone, a buy-and-build strategy can be effective in fragmented industries, allowing you to acquire smaller competitors that are a good fit for your platform. Just know that integrations can be challenging. You'll want to have a solid integration plan that allows you to mesh technology, back-office, and sales teams to unlock synergies for revenue growth and cost savings.

Talent Management and Incentives

Putting the right management team in place is critical. You structure management incentives around your investment thesis and key metrics. Skin in the game through equity compensation, options, or restricted stock are usually tied to EBITDA, revenue milestones, or exit proceeds. These incentives keep management thinking about building long-term value vs quarter-to-quarter earnings.

As for talent management, you want to make sure you have the right people around you. You hire experts (operations, technology, or commercial) with a track record of scaling similar businesses. You may even hire temporary gap management to maintain momentum while you find that unicorn.

PE Value Creation by Industry

Different industries reward different levers, and the smartest PE firms tailor their value creation playbooks accordingly.

- Healthcare: operational efficiency and private equity roll-up strategies dominate. Centralizing back-office, standardizing clinical protocols, and consolidating fragmented practice groups can unlock 200 to 400 basis points of margin expansion within the first 24 months.

- Technology and SaaS: buy-and-build plus digital transformation. Platform plays in vertical SaaS routinely use 8 to 15 add-on acquisitions to dominate niche markets, while operational alpha comes from converting on-prem revenue to ARR.

- Industrials: working capital management and lean operations. Tighter inventory turns and pricing discipline can free 5 to 20% of working capital, which often funds growth without new debt.

- Consumer: brand and pricing optimization, plus DTC channel buildout. Direct-to-consumer revenue streams typically command 1 to 2 turns higher EBITDA multiples at exit than traditional retail-only businesses.

Critical Tools, Metrics, and Best Practices

Private equity firms need to have clear frameworks and transparent metrics in place to deliver on value creation. This starts with conducting diligent research at the time of acquisition and continues with monitoring your portfolio with new tech and ESG factors in mind.

Due Diligence and Value Creation Planning

The work you do in the due diligence process will set the foundation for everything else. You analyze the target's operations, finances, market share, and growth opportunities to identify true opportunities for improvement. With those opportunities in mind, you can build your value creation plan. This plan will detail what you want to do, when you want to do it, and what you hope to accomplish. Remember to assign accountability, budget resources, and include measurable goals. Ideally, you want input from management, industry analysts, and operations experts. It's beneficial to agree on baseline metrics during due diligence so you can track if you are delivering on the deal thesis.

KPIs and Performance Measurement

Metrics are the dashboard that allows you to measure value creation. You should have a combination of financial and operational KPIs.

Financial metrics should include IRR, DPI, TVPI, and EBITDA growth. Internal rate of return (IRR) measures annualized return given the amount and timing of cash inflows and outflows, while multiple on invested capital (MOIC) shows total cash returned per dollar deployed. Top-quartile PE funds target 20%+ net IRR; the median PE fund returned approximately 13% net IRR over the last decade (PitchBook).

Operational KPIs will be more industry-specific but can include revenue growth, customer acquisition cost, retention, and margin expansion. Invest in technology that will allow you to measure these metrics on a real-time basis and compare them throughout your portfolio. Make sure your KPIs are aligned to your strategic objectives and the value levers you identified earlier. Frequent check-ins will allow you to pivot your strategy and course correct if needed.

Technology, Innovation, and ESG Factors

Digital transformation is likely one of your highest value levers right now. Through data analytics and machine learning, you can identify operational bottlenecks, price yourself optimally, and forecast more accurately. Automation of processes, streamlining your supply chain, and improving CRM software all fall under technology improvements. Focus on ways to improve operating efficiency and scalability.

“If you're not at least somewhat technology-enabled, you'll struggle to stay relevant as an operating partner.”Aaron Miller, Partner and Head of Apollo Portfolio Performance Solutions (APPS), Apollo Global Management, speaking at the PEI 2025 Operating Partners Forum.Apollo's APPS team treats tech enablement as table stakes for every new portfolio company, not a discretionary upgrade. The implication is plain: operating partners who cannot translate AI, data analytics, and automation into measurable EBITDA gains will be replaced by those who can.

ESG considerations should be integrated into any operational improvements you plan on making (carbon footprint reduction, governance, social impact, and similar). Many investors will have ESG screening criteria when looking at targets, and those factors can play into your returns. Plus, getting ESG right can help you build a stronger and more defensible position in the market while helping mitigate risk.

Exits, Returns, and Real-World Examples

Exit is where the rubber meets the road for private equity value creation. This is when firms exit their investments and see if their operational improvements actually created value. If the exit valuation is high enough (especially with multiple expansion), then it can demonstrate that real value was created and it wasn't just financial engineering.

Identifying Exit Opportunities

First, know that there is no set time for the perfect exit window. Market conditions, company performance, and buyer demand can shift the ideal timing for years or even months. Some PE firms have an exit plan as early as year one of ownership, sometimes even before they begin operational improvements.

Historically, hold periods ranged from three to seven years, but 2025 data shows median holds have lengthened to 6 years and average buyout holds to 6.4 years (S&P Global, 2025). This varies widely based on the needs of the company and market conditions.

Establishing a competitive market position and focusing on brand equity during your time of ownership helps differentiate your company from others for buyers. Private equity buyers are also savvier these days. They will conduct thorough due diligence and want to see evidence of your value creation. Digital transformation and ESG are other value drivers that are top of mind with buyers. If you're looking to sell for a premium, don't ignore these items.

There are typically three exit paths: strategic, other PE firms, or public markets. Each exit path has different preparation needs.

Valuation, Multiples, and Profitable Exits

How much you sell for will largely be dictated by your revenue, profitability, and operational efficiency built throughout your ownership. If you sell for a higher EBITDA multiple than you bought it at, this is called multiple expansion. Multiple expansion at exit is the highest-leverage outcome, but it has to be earned through operational improvement, not borrowed from market timing.

The three largest drivers of profitable exits are typically EBITDA growth, multiple expansion, and debt paydown throughout your ownership. An IPO allows you to access liquidity and participate in future upside. Another strategy is to do a recap and take out some capital, leaving with an ownership stake in the company. To go public, you need to have a certain level of financial performance, corporate transparency and governance, as well as scalability to attract public market investors. It's not the right path for every company, but can be the ideal exit for some.

Case Studies and Lessons Learned

Standardized products, normalized margins, and control of working capital drove operational value creation in Carlyle's 2004 AZ Electronic Materials (AZ-EM) investment. Debt used to fund the acquisition was paid back by management within three years. Carlyle sold a majority stake in the business to Vestar Capital for €1.4 billion at a 10x multiple.

“A return to first principles: revenue growth, operational excellence, and innovation.”Paul Vega, Partner at Cinven, in an interview with ION Analytics describing how the firm approaches value creation in today's environment.The firm's earlier investment in Phadia is a textbook example. Investments from Cinven allowed Phadia to expand into adjacent products to drive growth. During Cinven's ownership, Phadia introduced next-generation allergy and autoimmunity testing systems capable of much higher throughput than existing competitors, growing from just €96 million to €146 million in EBITDA in the midst of a recession. Sold to Thermo Fisher in 2011 for €2.47 billion, Cinven walked away with approximately $1 billion in profit and a 3.4x return on investment.

Summit Partners used a buy-and-build strategy to grow Infor, completing nine acquisitions that helped shift its business to the cloud. By 2017, cloud applications represented more than 50% of total revenue. Infor was sold to Koch Industries in 2020 for approximately $13 billion, one of the largest tech buyouts of the decade and a textbook buy-and-build outcome.

Why PE Deals Fail to Create Value

Even with the right diligence and a smart VCP, a meaningful share of private equity deals fall short of their underwritten returns. Understanding why is essential whether you're on the buy-side, the sell-side, or running a portfolio company today.

There are five recurring causes of value creation failure:

1. Governance structure failures. Boards organized purely along functional lines (CFO, COO, head of sales) leave no one accountable for cross-functional initiatives, and integration projects are exactly that.

“There are typically a few reasons why deals go wrong. One of them is that there's a lack of a definitive governance structure to the cross-functional model. All the governance structures are built towards the functional side of it, and that creates a problem.”Nitin Kumar, a seasoned C-level operating executive and management consultant in the technology, media, and telecom (TMT) sector.2. Misaligned incentives between deal teams and operators. The corp-dev professionals who source a deal often hand off to a sponsoring business unit and an integration management office (IMO) without a clear chain of accountability.

“The machinery between the corp-dev people, the sponsoring business unit, and IMO are typically not well-defined and aligned on who is responsible for the success of the deal and creating that shareholder value.”Nitin Kumar, continued.3. Integration breakdowns. Buy-and-build strategies fail most often during the integration of acquired add-ons rather than the platform thesis itself. Common failure modes include cultural mismatches, technology stack consolidation overruns, and customer attrition during rebrand or rebill cycles.

4. Management team mismatch. The best operator for a $50M business is rarely the best operator for the same business at $250M. Funds that hold leadership too long, or replace too quickly, both pay a price.

5. Over-leverage in a rate-rising environment. Capital structures sized for 4% rates buckle when rates climb. Deals closed in 2020 to 2022 at peak multiples and minimum spreads are now showing the strain in 2025 hold extensions and amend-and-extend negotiations.

Avoiding these failure modes is what separates top-quartile funds from the median. The execution discipline matters more than the strategy.

Frequently Asked Questions

Private equity value creation is less financial engineering these days and more operational improvement, strategic repositioning, financial engineering, and talent optimization. Returns measures, strategies, and skills have changed as the marketplace has become more competitive. Operational expertise is more important now than it has ever been.

How do PE firms create value?

Value is created by working in portfolio companies rather than sitting on the sidelines. PE firms collaborate with management to implement strategic, operational, and financial improvements while holding companies. This typically involves getting down into the trenches and making data-driven decisions. You identify opportunities through due diligence and execute on changes to operations, strategy, and capital structure.

What are three value drivers of private equity firms?

Operating, financial, and strategic initiatives. Operations tactics focus on improving EBITDA via cost savings, top-line growth, and operational adjustments. Leverage allows you to earn returns on the debt you bring to the table when financing deals. You pocket the spread between your cost of debt and return on equity. Multiple arbitrage and digital transformation initiatives round out the strategic dimension. Technology is implemented to create operational efficiencies, improve customer experience, and enhance data-driven decision making.

What is the difference between operational and financial value creation?

Operational value creation grows EBITDA by improving how the business actually runs through better pricing, leaner operations, sharper sales execution, and smarter capital allocation. Financial value creation grows equity value by changing the capital structure through leverage, refinancing, or multiple expansion at exit. They overlap because financial moves only work when the underlying business is sound, and operational improvements only translate to investor returns when the capital structure captures them.

What skills do you need for value creation jobs in private equity?

Operational expertise and financial acumen are table stakes for value creation. This translates to proficiency in how businesses operate, manage supply chains, and drive performance in various sectors. Data analytics chops are increasingly valuable as well. Being able to interpret stochastic modeling, predictive analytics, and alternative data can help you identify opportunities for impact. Change management and leadership skills are also critical. After all, if you can align portfolio management teams with the business, your value creation projects stand a greater chance of success.

How has private equity's focus on value creation changed over the years?

Years ago it was financial leverage, multiple arbitrage, and top-line growth, aided by lower interest rates. It was okay to be half-asleep on the ops side if the wind was at your back. Today, with less tailwind, there is no better way to differentiate than through operational alpha. Think systematic and rapid cycles of EBITDA improvement rather than financial engineering. In fact, many top-quartile PE firms are adopting quantitative techniques borrowed from hedge funds, including outside-in market signals, predictive analytics, and stochastic modeling, to replace gut-feel underwriting and conventional financial-only metrics.

How is value creation measured for PE investments?

Value creation in private equity is measured primarily by EBITDA growth during the hold period, multiple expansion at exit, and debt paydown. Internal rate of return (IRR) and multiple on invested capital (MOIC) capture the overall financial outcome, with top-quartile funds targeting 20%+ net IRR. Operational KPIs such as revenue growth, gross margin, customer acquisition cost, and retention track the underlying business improvement that ultimately drives those returns. More recently, top-quartile firms also track speed of value creation, often focused on the EBITDA gains delivered in the first 100 days of ownership.

Key Takeaways

- Private equity value creation is the process of adding value to your portfolio companies through operational, financial, and governance improvements to ultimately enhance investor returns.

- Instead of relying solely on financial leverage to create value, many modern firms are focused on sustainable, data-driven operational improvements. The 59% of returns that came from leverage and multiple expansion in the 2010 to 2022 era is no longer available.

- Bain's '12 is the new 5' framing captures the new bar: PE firms now need approximately 12% annual EBITDA growth to deliver historical 2.5x returns over five years.

- Leading firms differentiate themselves by having the proper tools, metrics, and execution capabilities to manufacture operational alpha.

Execution is where private equity value creation is made or lost. Top-performing firms succeed because they execute on initiatives beyond just financial levers. But far too many deals fall short on execution due to disjointed tools, unclear ownership, and siloed transparency.

The DealRoom M&A Platform bridges those gaps with a central platform for your M&A diligence, integration planning, and value creation activities. Teams can map initiatives, assign owners, and monitor KPIs in real time. Request a demo to see DealRoom in action.